In African dealmaking, macro is not background noise. Macro is the weather system. Ignore it and your project finance model becomes fiction.

The Common Cycle

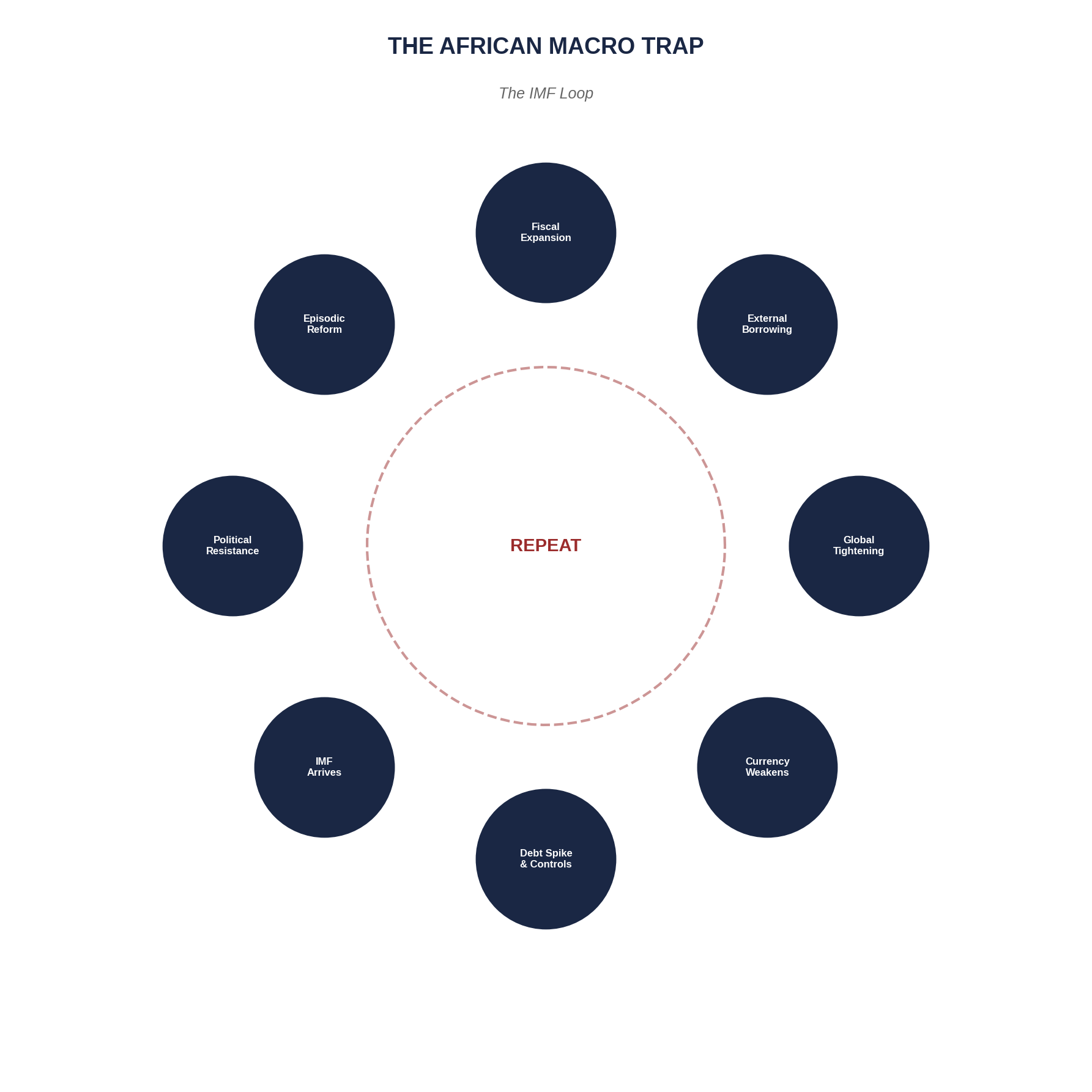

The pattern is predictable:

The macro cycle that breaks deals: from fiscal expansion to IMF conditionality.

- Fiscal expansion outruns revenue

- External borrowing grows (often in foreign currency)

- Global conditions tighten; refinancing costs spike

- Currency weakens; debt service explodes

- Controls and arrears expand

- The IMF arrives with financing and conditionality

- Politics resists adjustment

- Reform becomes episodic

Since 2020, Ghana, Zambia, and Ethiopia have all entered debt restructuring. Kenya has narrowly avoided it through repeated fiscal tightening. Nigeria manages through currency rationing. Egypt cycles through IMF programmes with predictable regularity.

Zambia: The Program Arc

Zambia defaulted in November 2020. Its Extended Credit Facility with the IMF was approved in August 2022, with disbursements contingent on debt restructuring progress. By late 2024, Zambia had completed restructuring with bilateral creditors and was advancing bondholder negotiations.

The pattern illustrates what serious investors expect: sovereign stress forces discipline, discipline restores confidence, confidence lowers the cost of capital. But the cycle is measured in years, not quarters. For project developers with construction timelines, this is duration risk that must be priced.

What Macro Stress Does to Deals

Macro stress reliably causes:

- Foreign exchange rationing and delayed transfers

- Payment arrears, especially where the state is an offtaker

- Surprise taxes and "temporary" levies

- Slower approvals

- Political interference in regulated pricing

The lesson for investors is brutal: when macro breaks, micro deals suffer. When foreign exchange is scarce, legal rights become negotiation tools.

Structuring for Macro Reality

Smart capital stops pretending that "project finance" is purely project-specific. It underwrites sovereign and currency risk as first-class variables:

- Revenue and debt currency matching wherever possible

- Debt service reserve accounts—funded buffers for repayments

- Offshore escrow waterfalls with hard-coded payment priority

- Step-in rights that define lender control under specified defaults

- Political risk allocation documented in term sheets, not assumed in projections

The IMF loop is not a reason to avoid Africa. It is a reason to structure like an adult.

This is Part 6 of a 10-part series on African investment, state capacity, and capital allocation.

Previous: ← Part 5: Return-on-Risk