Return-on-risk is the probability-weighted ability to deploy capital, operate without fundamental disruption, and repatriate returns in hard currency. It is not GDP growth. It is not market size. It is the unromantic question: if I build, buy, or lend, what is the probability I get my money out—legally, on time, at a predictable cost?

The Five Variables That Dominate

Currency regime credibility: Not whether the currency is "strong," but whether the system is coherent. Can you convert local earnings to dollars at a known rate? Can you access that rate reliably?

Capital repatriation mechanics: Can dividends, interest, and principal be transferred without delay? Are the rules published and enforced?

Contract enforcement: Disputes are inevitable. The question is whether the system converges to resolution—through courts, arbitration, or credible sovereign honour.

Sovereign interface risk: Taxes, permits, licences, and regulatory discretion. Often the real killer of project timelines.

Shock absorption: How the system behaves under stress. Does it tighten controls, rewrite rules, or protect predictability?

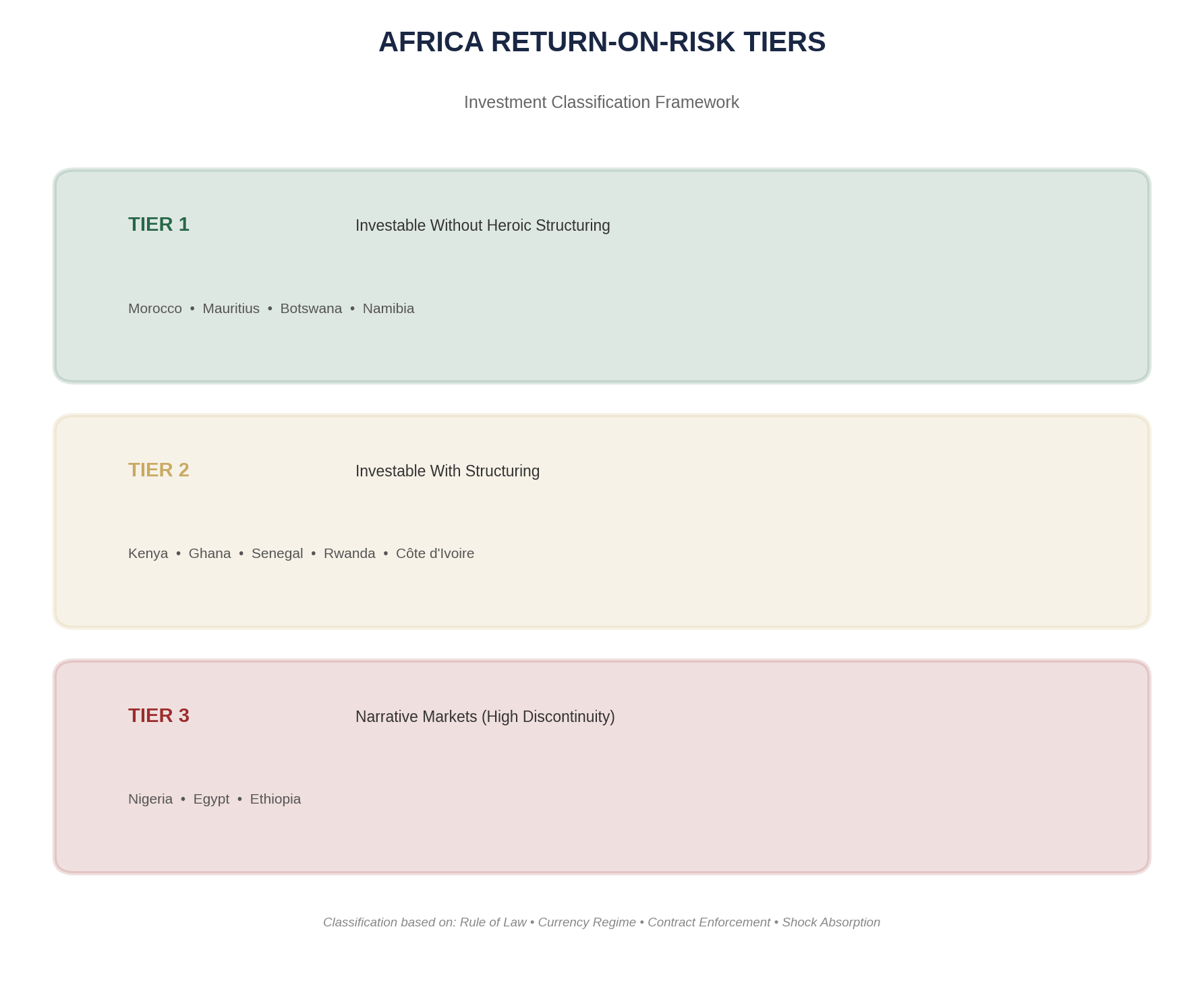

The Tier System: A Practical Framework

Investment tier classification based on return-on-risk, not GDP growth.

Tier 1 — Investable without heroic structuring: Morocco, Mauritius, Botswana, Namibia. These markets have enough rule-of-law infrastructure that standard transaction documentation works. Returns may be lower, but execution risk is materially reduced.

Tier 2 — Investable with structuring: Kenya, Ghana, Senegal, Rwanda. These markets offer higher returns because they require real advisory work: ring-fenced cash flows, offshore escrows, step-in rights, and covenants that assume politics will test the contract.

Tier 3 — Narrative markets: Nigeria, Egypt, Ethiopia. Returns exist, but underwriting must assume discontinuity. Tenors shorten. Risk allocation becomes binary. These are trading venues, not compounding destinations—unless offshore cash flows are achievable.

Case Study: Ghana's Tema Port Expansion

Ghana's Port of Tema handles 85 per cent of the country's trade. The Meridian Port Services Terminal 3 expansion—a public-private partnership with the Ghana Ports and Harbours Authority—illustrates Tier 2 structuring in practice.

In 2022, the operator signed a $53 million agreement for phase two expansion, adding fifteen gantry cranes. The project succeeded because it was structured as a concession with dollar-denominated revenue (port tariffs), offshore collection accounts, and lender protections that survived Ghana's 2022 debt crisis.

Meanwhile, Ghana's broader PPP pipeline remains underutilised. Experts note that while Kenya, South Africa, Morocco, and Côte d'Ivoire have mobilised billions through PPP frameworks, Ghana operates "far below its capacity." The country's infrastructure deficit is estimated at $37 billion annually over the next three decades. The Tema success shows what is possible; the broader underperformance shows what is typical.

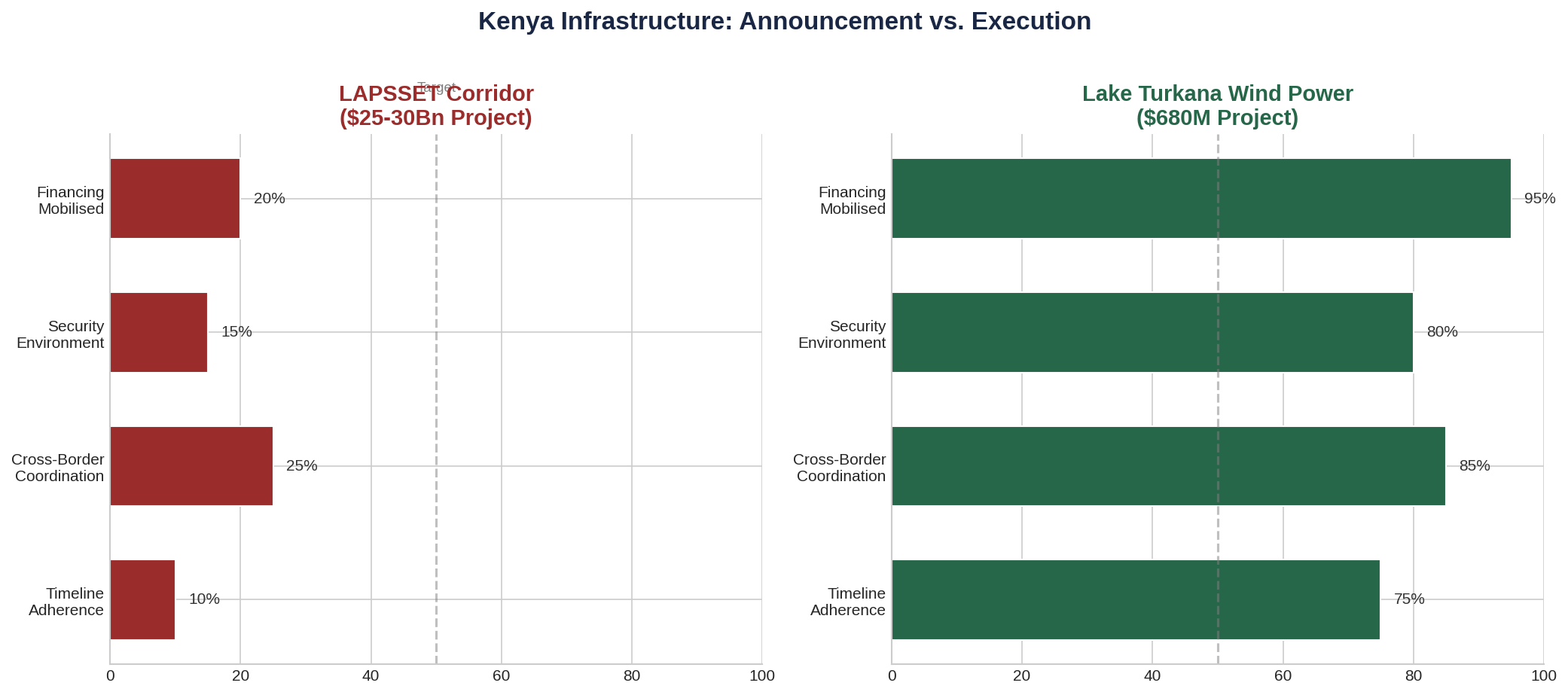

Case Study: Kenya's Lake Turkana Wind Power

The difference between announcement (LAPSSET) and execution (Lake Turkana).

Lake Turkana Wind Power, at 310 megawatts, is Africa's largest wind farm and the single largest private investment in Kenya's history at approximately $680 million. Today it provides nearly 17 per cent of Kenya's installed capacity.

The project succeeded not because Kenya is "investable" in the abstract, but because sixteen institutional partners—including development finance institutions, commercial lenders, and equity sponsors—structured around every identified risk:

- Political risk insurance from development finance institutions

- Ring-fenced power purchase agreement with Kenya Power

- A dedicated 438-kilometre high-voltage transmission line

- Offshore escrow mechanics for debt service

- Step-in rights for lenders under defined defaults

The Contrarian Truth: Tier 2 Can Outperform

The best risk-adjusted returns are often earned in Tier 2 markets—where risk is real but structurable. This is where serious advisory earns its fees: not in creating narratives, but in building transaction architecture that survives stress.

Return-on-risk is not about avoiding Africa. It is about refusing to confuse optimism with underwriting.

This is Part 5 of a 10-part series on African investment, state capacity, and capital allocation.

Previous: ← Part 4: Countries Moving Backwards