Africa is ranked to death. Fastest-growing region. Youngest population. Most promising frontier. Best reformers. And yet, after three decades of rankings, reports, and investment roadshows, one fact persists: very little long-term, compounding capital sticks.

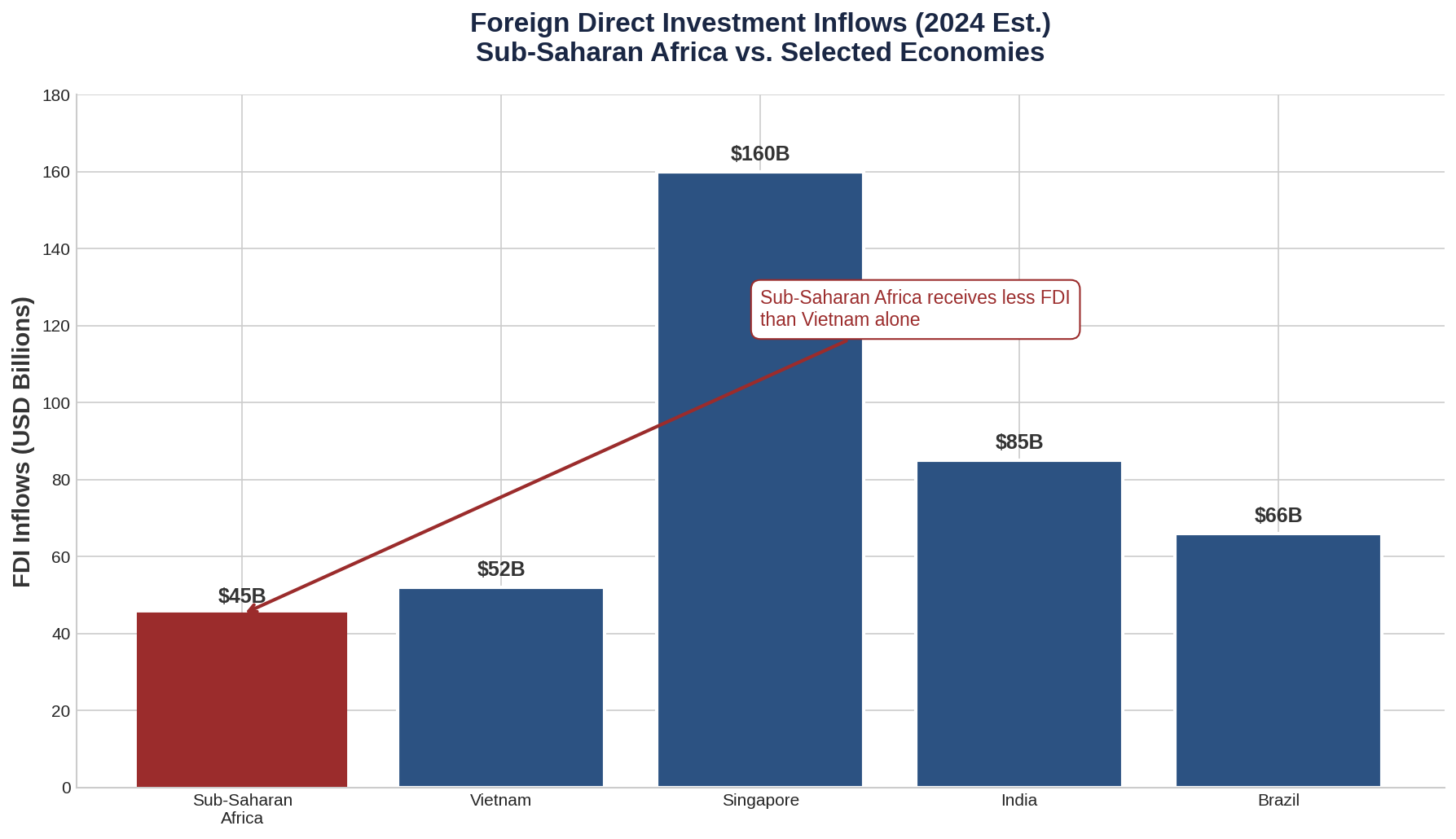

Consider the arithmetic. In 2024, sub-Saharan Africa received approximately $45 billion in foreign direct investment—less than Vietnam alone. The region's share of global FDI has declined over the past decade even as its population has grown by 300 million. The few megadeals that do occur cluster in extractives, often structured to minimise in-country value addition and maximise repatriation optionality.

Sub-Saharan Africa receives less FDI than Vietnam alone, despite having 15 times the population.

This is not a marketing failure. It is a measurement failure. Most Africa rankings are designed for donor comfort, not capital survival. They reward outcomes—GDP growth, population size, optimism indicators—while ignoring the only variable that predicts whether outcomes persist: state capacity.

Kenya's Infrastructure Paradox

Kenya offers a useful case study in what rankings miss. By most indices, Kenya ranks among Africa's top ten investment destinations. It has East Africa's deepest capital markets, a sophisticated private sector, and genuine infrastructure ambition. Yet examine the execution record, and a different picture emerges.

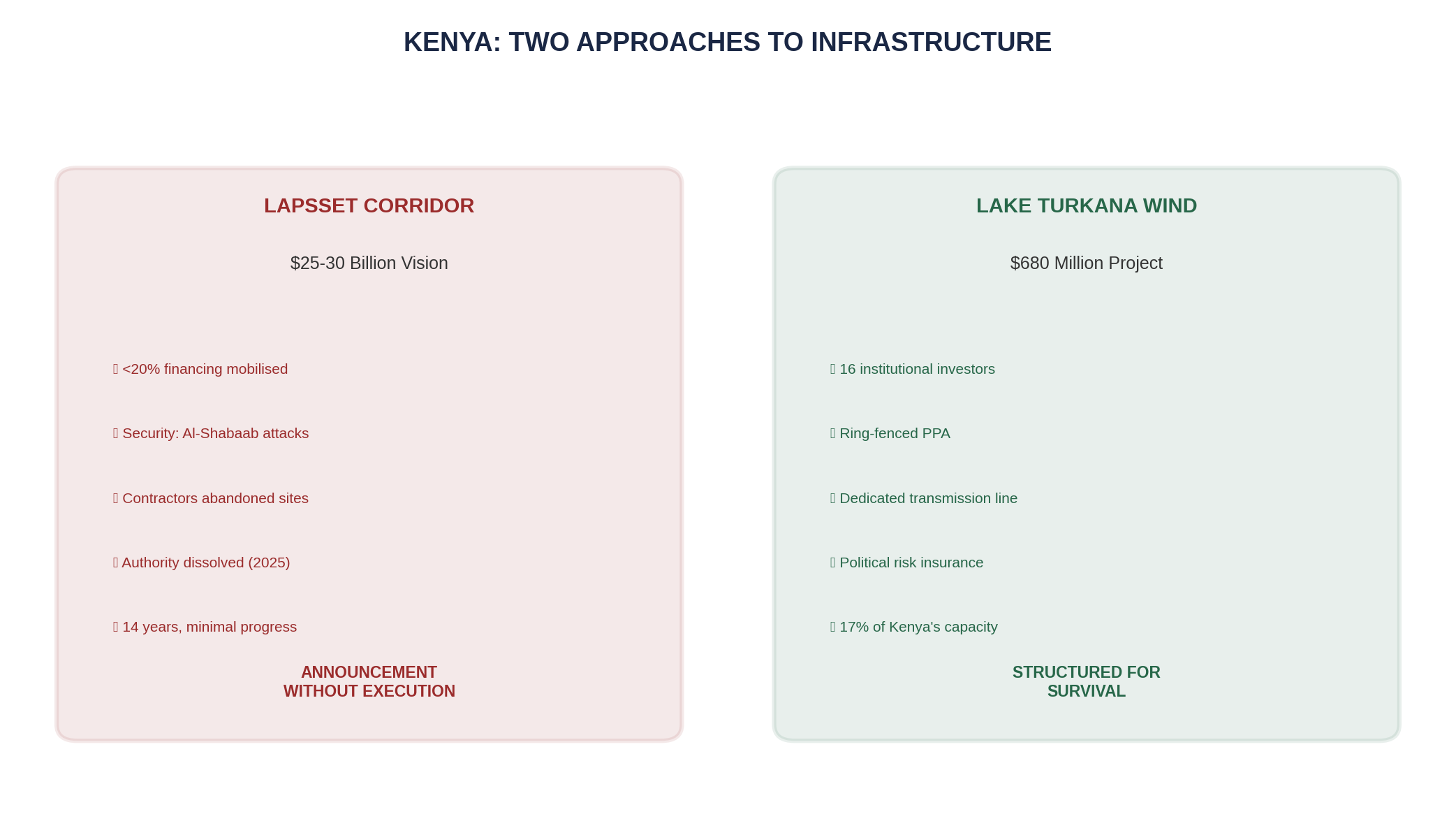

Two approaches to infrastructure: LAPSSET's announcement model versus Lake Turkana's execution model.

The Lamu Port-South Sudan-Ethiopia Transport Corridor (LAPSSET) was announced in 2012 as a $25–30 billion transformative project—a port, highways, railways, pipelines, and resort cities linking Kenya to Ethiopia and South Sudan. Fourteen years later, the project has mobilised less than 20 per cent of required investment. The Auditor General's 2024 report confirmed that "construction of key highways is either not completed or is yet to start." Chinese contractors have periodically abandoned sites due to Al-Shabaab attacks. The LAPSSET Corridor Development Authority itself was dissolved in 2025, its functions absorbed into line ministries.

This is not bad luck. It is a capacity constraint. The Kenyan state announced a project it could not protect, finance, or coordinate across three countries with divergent interests. The vision was real; the conversion machinery was not.

Compare this to Lake Turkana Wind Power, completed in 2019 after years of delay but now supplying 17 per cent of Kenya's installed capacity. The difference was not ambition—it was structure. A consortium of sixteen institutional investors, development finance institutions with political risk coverage, a ring-fenced power purchase agreement, and a transmission line built specifically to evacuate the power. The project succeeded because it was underwritten for survival, not for announcements.

Growth Is Often Borrowed Time

Five per cent GDP growth can coexist with unsustainable fiscal deficits, foreign-currency debt accumulation, and exchange rate distortions. When adjustment arrives—as it did in Ghana, Zambia, and Ethiopia—the growth evaporates. The losses remain.

Ethiopia grew at an average of 9.4 per cent annually for over a decade. It was celebrated as Africa's lion economy. Yet by December 2023, Ethiopia became the third African sovereign in two years to default on its Eurobond, following a $33 million coupon miss. The country entered the G20 Common Framework for debt restructuring, where it remains—as of January 2026—unable to finalise terms with private creditors due to disputes over "comparability of treatment" with official creditors.

Growth without capacity is noise. Rankings that ignore this are selling a product, not underwriting a thesis.

What Capital Actually Wants

Capital does not fear risk. It fears unpriced risk—the kind that arrives as policy reversal, currency rationing, sudden taxes, contract disputes, or an administrative state that forgets what it signed.

The 2024 Adani airport controversy in Kenya illustrates this precisely. In March 2024, Adani Enterprises submitted an unsolicited proposal to operate Jomo Kenyatta International Airport for 30 years in exchange for $1.85 billion in investment. The proposal bypassed competitive bidding. It remained secret until leaked on social media in July. When scrutinised, the Kenya Airports Authority found the feasibility study "untenable." The Kenya Human Rights Commission and Law Society of Kenya sued. Airport workers struck. And in November 2024—after Adani's founder was indicted in the United States on bribery charges—President Ruto cancelled the deal entirely, along with a separate $736 million power transmission contract.

The Adani saga was not primarily about Adani. It was about process. A $2.6 billion infrastructure commitment was negotiated in secret, announced without scrutiny, and cancelled within months. For institutional capital, this is not "political risk"—it is structural unpredictability. And structural unpredictability cannot be priced; it can only be avoided.

Africa does not need better narratives. It needs boring competence—clear rules, credible enforcement, predictable exits. These are not moral virtues. They are infrastructure, just as real as roads.

Sources

- LAPSSET Project Status - The Star Kenya

- Lake Turkana Wind Power - Official Site

- Ethiopia Debt Restructuring - Addis Standard

This is Part 1 of a 10-part series on African investment, state capacity, and capital allocation.

Next: Part 2: State Capacity →